The question is relevant at this time when the Bill amending the consolidated text of the Capital Companies Act and other financial regulations is currently undergoing parliamentary proceedings. This amendment responds to the transposition into our legal system of EU Directive 2017/828 to promote the long-term involvement of shareholders in listed companies. The purpose of this directive is to promote greater shareholder participation in the corporate life of issuers, and at the same time to avoid short-term and speculative behavior, both on the part of listed companies and investors, which generate inefficiencies in the market, compromise the economic sustainability of the former, and, ultimately, produce a destruction of long-term value.

One of the most striking aspects of the modification will involve the freedom of decision for listed companies whether or not to publish financial information on quarterly results, specifically the one corresponding to the first and third quarters of each financial year, since the biannual and annual periods will continue to be mandatory. This, although a priori it may seem like a positive change, nevertheless opens up a risk of losing information transparency in the markets, which in my opinion is unnecessary.

Without going into the assessment of the reasons given by the regulatory bodies to carry out this modification, I am however interested in writing down some reflections regarding the context in which this modification will take place and its consequences.

In 2016, the president of BlackRock, Larry Fink, said in his annual letter to the CEOs of the main investors: “The current culture of hysteria over quarterly results is totally contrary to the long-term approach we need. We believe that companies have an obligation to be open and transparent in terms of sharing their growth plans, so that shareholders can value them [...].”

It is paradoxical that precisely the directive that gave rise to this change was called the Transparency Directive, whose possible consequence is that the market, i.e. analysts and investors, is faced with a vacuum of relevant information on the evolution of the management of listed companies for a period of time of up to six months.

In 2016, the president of BlackRock, Larry Fink, in his annual letter to the CEOs of the main North American and European companies, expressed his concern precisely about the short-term strategies that some companies were carrying out with the objective of maximizing the price. In that writing, he even added literally: “the current culture of hysteria over quarterly results is totally contrary to the long-term approach we need. We believe that companies have an obligation to be open and transparent in terms of sharing their growth plans, so that shareholders can assess them, as well as the degree of progress in executing those plans.”

Can we infer from the letter from the world's leading institutional investor that his recommendation to the first executives of issuers was to stop publishing quarterly earnings reports? In my opinion not at all, and I think that the debate is poorly focused in terms of the frequency of publication, when it should be about the convenience or not of providing guidance or Guidance to the market with respect to short-term objectives such as three months ahead.

It is reasonable to think that it is precisely the practice of some listed companies of disclosing these short-term objectives that generates a speculative spiral among investors, and anxiety among issuers to meet expectations, which can lead to serious management errors in order to beat them, to the detriment of long-term growth.

Involving shareholders in the long term involves, among other things, facilitating their understanding and monitoring of the company's activity and business model, and this is achieved through a Equity Story focused and updated in a systematic way, and with a Reporting quarterly quality report to identify the company's progress in the direction outlined by the long-term corporate strategy. El Reporting quarterly can never be a substitute for transparency, but rather a tool to promote it.

At this point, it is worth remembering the correct recommendations published by the CNMV in January 2012 on the content of the Quarterly Financial Information to guide listed companies in the application of Article 120 of the consolidated text of the Securities Market Act on the so-called interim management statement (financial reports for the first and third quarters), which will soon be repealed.

However, a lot has changed since then, both the market environment and the information needs of investors, so that, in my opinion, they have left these recommendations short. Aspects such as capital management and indebtedness are areas of management increasingly monitored by investors, as well as non-financial information, not only that relating to lines of business and perhaps geographical markets, but also that relating to the activity of listed companies with environmental, social and corporate governance (ESG) impacts. If we also talk about companies that are in a profound phase of transformation or growth, the absence of management information for a long time can represent a lost opportunity to attract or attract capital or even a generator of volatility, and therefore an increase in their cost of capital.

It would be desirable for the experience of the British market, [...] not only to be replicated in our country, but also Companies that today place their level of compliance at the legal minimum are encouraged to take advantage of the opportunity to increase the reach of their information on a recurring basis

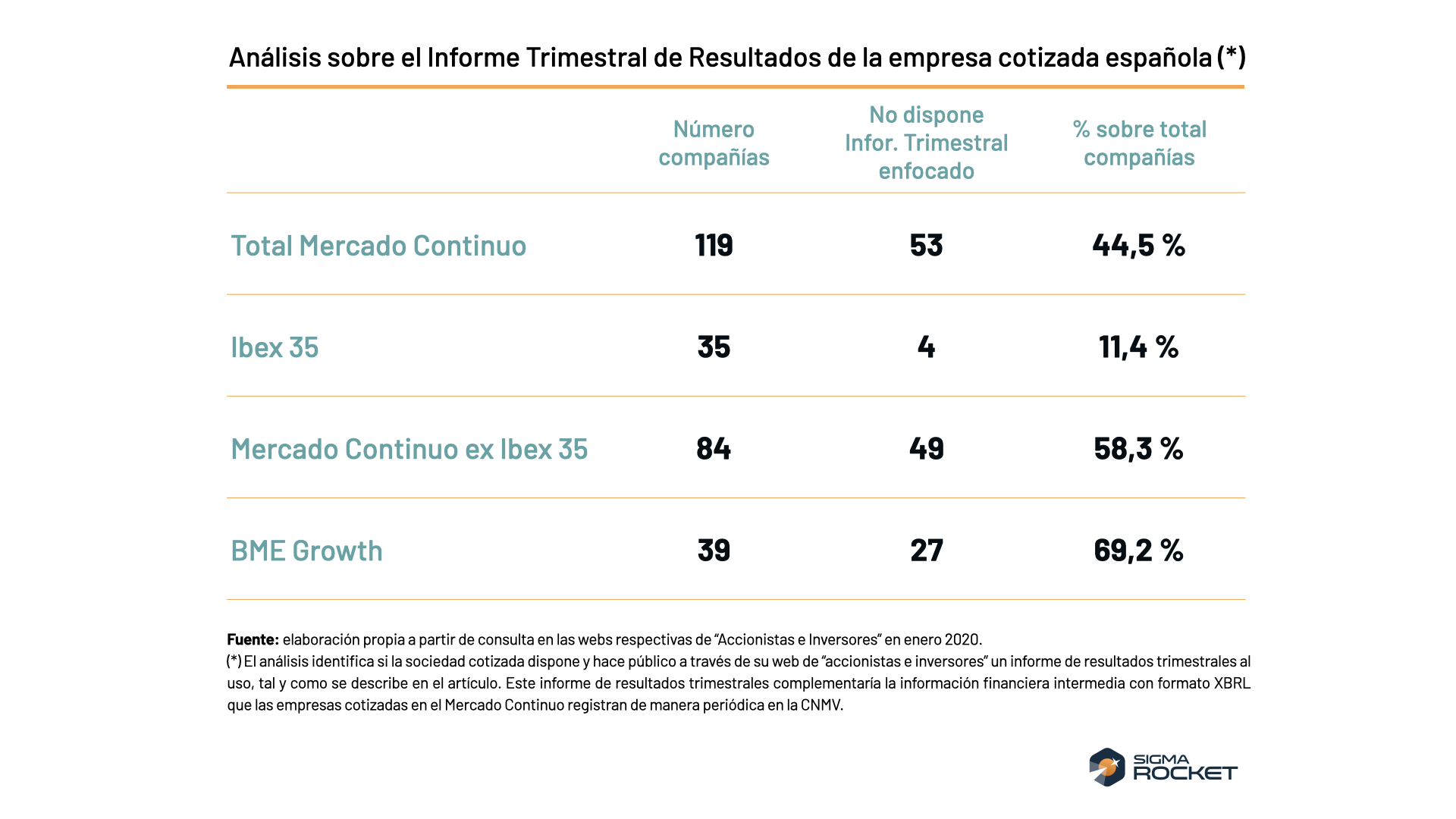

If we analyze the situation of the Spanish listed company with respect to what we can consider a quarterly earnings report as usual, that is, a report with the complete financial statements, including the statement of cash flows, an adequate narrative describing the evolution of management from the company's perspective to facilitate the understanding of the figures, the publication of non-financial indicators with special attention to those relating to lines of business and geographical markets, if that is the case, and even the management information or most relevant metrics in terms of ESG, we can conclude that there is a clear opportunity to improve the quality and depth of the Reporting quarterly, as can be seen in the following table, the result of the analysis of the information available through the respective “Shareholders and Investors” web space.

Therefore, renouncing quarterly disclosure would seriously damage transparency and information available to investors, with inevitable consequences on the valuation of listed companies. It would be desirable if the experience of the British market with the minimum incidence of change since its approval in 2014, barely 10% stopped publishing quarterly information, not only to be reproduced in our country, but also that companies that today place their level of compliance at the legal minimum are encouraged to take advantage of the opportunity to increase the reach of their information on a recurring basis.

It is not a question of generating paralysis through analysis based on the communication policies of companies, but of making it easier for investors to understand business and to form expectations. Warren Buffet once commented that accounting is only the beginning and not the end of the valuation of a company or a business, to which I would add that, in any case, it is a good starting point.

-

Francisco Blanco Bermúdez

Founding partner of Sigma Rocket