As we approach the end of the first quarter of 2021, companies in the Continuous Market have just released their 2020 results report. Some of them have even taken advantage of the year-end communication to share their estimates for the current new year. Provide the market with forecasts of future results, more commonly known by the Anglo-Saxon term of”Guidance”, is a delicate issue and also one of trust. In fact, investors and analysts, as soon as they have such guidance from the listed company, will scrutinize the sustainability of these estimates with each future communication of results or relevant events that affect their expectations. In this regard, the consistency with which the forecasts have been formulated, and their compliance, will greatly condition the credibility of the management team and the company before investors.

The question that the company could then ask itself is whether or not it is appropriate to give guidance to the market as part of its expectations management strategy. The answer is not simple because it depends on several factors, such as the level of practice of its Investor Relations policy, the degree of complexity of the company's business model in providing analysts and investors with sufficient understanding to make realistic projections, or the number and importance of exogenous factors that impact its results, and that therefore do not depend on its management.

All of these factors largely determine whether a company is more or less predictable in the eyes of the investor or analyst, and this is a key question to know to what extent it is necessary to “guide” the market.

Many companies understand that to help investors in their investment decision, a transparent and proactive Investor Relations policy based on reporting on events is not enough, but that it is also necessary to complement this information with future forecasts of their activity (Copeland and Dolgoff, 2005).

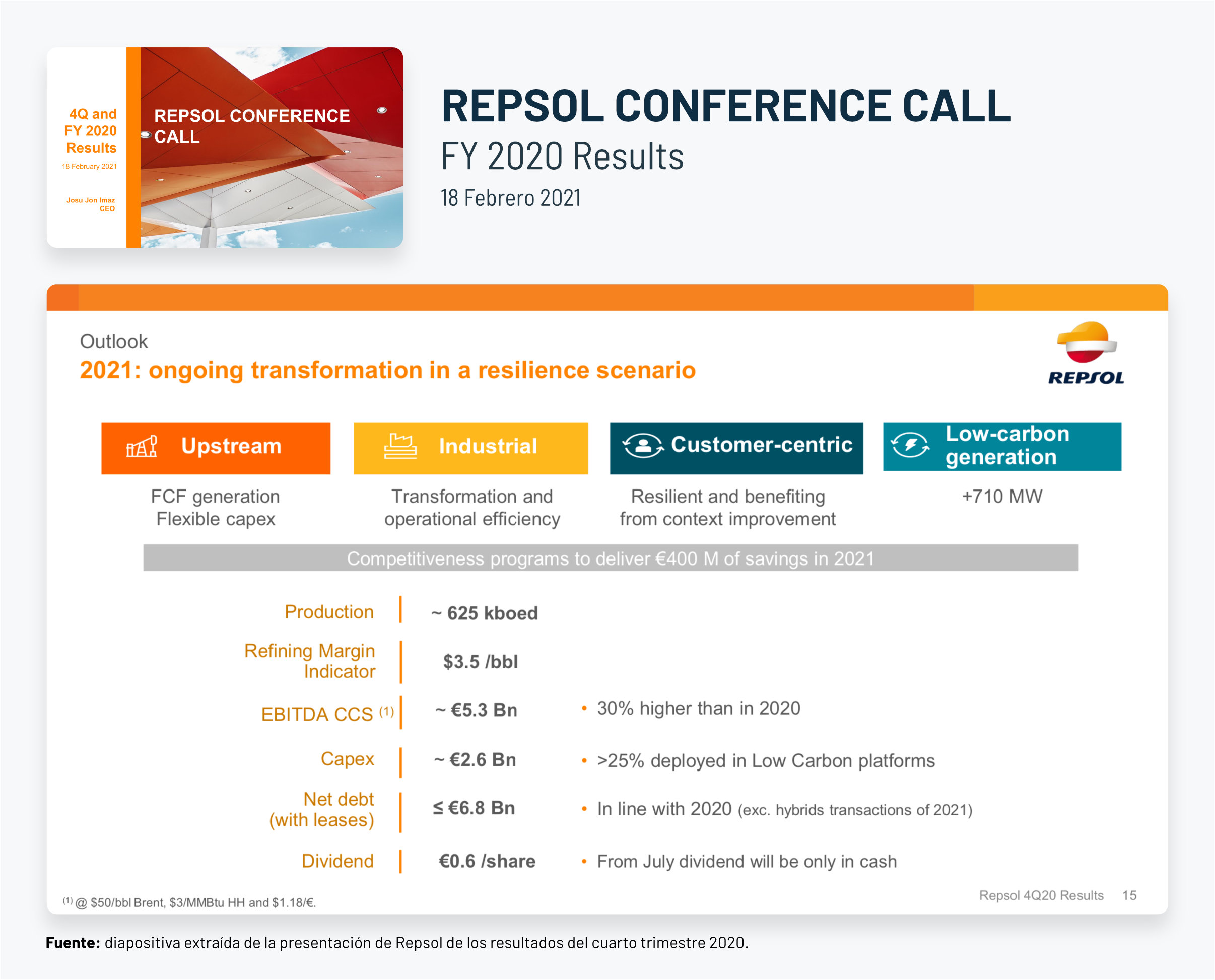

Two clear examples of companies recognized in the European field of Investor Relations for their proactivity and level of predictability are the German chemical company Basf, and the Spanish energy company Repsol. As can be seen in figure 1, in both cases, the Guidance that they share with the market for 12 months or the medium term refer to very specific financial indicators such as the generation of EBITDA and free cash, the investment program (CapEx), the level of indebtedness, or the shareholder compensation policy. In turn, these types of projected metrics are complemented by an extensive explanation and documentation of their business model and future strategy at the corporate level and of the different business units without the need to establish detailed numerical projections of them.

However, under certain circumstances, the need to deepen or provide more detail about the company's expected operational and financial developments may be greater if we want to avoid a high dispersion of analysts' estimates, and thus additional volatility.

A recent example of this situation was the significant communication effort made by Repsol at the end of last year on the occasion of its Investor Day, in which it addressed the project to transform its operating model as a firm commitment to becoming a leading player in the renewable energy sector (figure 2). Throughout the different presentations that took place during the day, it was possible to see a notable opening of Repsol to provide the market with a better understanding of the different aspects of the development of the new operating model and its implications with respect to value. An exercise aimed at building trust and credibility.

With regard to providing projections to the market, either through the numerical quantification of certain operational or financial metrics, or through the setting of percentage ranges of their expected evolution, the standards of good practice agree on the following recommendations (Finno and Brush, 2013):

i) Any estimate that is shared with the market must be recovered in future editions of the Equity Story to assess the degree of compliance achieved with respect to their actual values.

ii) The methodological criteria used to define metrics or parameters must have continuity over time to facilitate the comparability and consistency of the values.

iii) The time horizon of the projections will depend on the circumstances of the company, and on the characteristics of the industry to which it belongs; in any case, it is more recommended that it be placed in the long term than in the short term due to the greater additional volatility that can be generated around short-term projections and the price on the dates close to the reporting of quarterly results.

iv) Forecasts must set attainable objectives, and in no case should they seek to generate artificial movements in the price.

In this regard, it should be noted the importance for the company to take the initiative in setting expectations that serve as an orientation to the market and not the other way around. In fact, with this type of action, situations such as the one that happened in the case of Enron at the beginning of the first decade of this century could have been avoided. At that time, the North American energy company was subject to market pressure to set its own budgetary objectives in an environment characterized by the asymmetries of information available between investors and analysts, and their excessive short-termism focused on the publication of the next quarterly results.

In this expectation-formation model called “The Earnings Game”, the management team of the company involved communicates on a recurring basis those quarterly or annual results objectives that satisfy the market, and then makes operational and financial decisions to ensure that these short-term objectives are met regardless of their sustainability or generation of unfounded expectations, creating a speculative bubble (Copeland and Dolgoff, 2005).

In the case of Enron, this process of setting internal objectives, which was ultimately perverse to the interests of the company and the shareholders themselves, led the management team to malpractices, including market abuse and manipulation of financial statements in order to meet analysts' expectations.

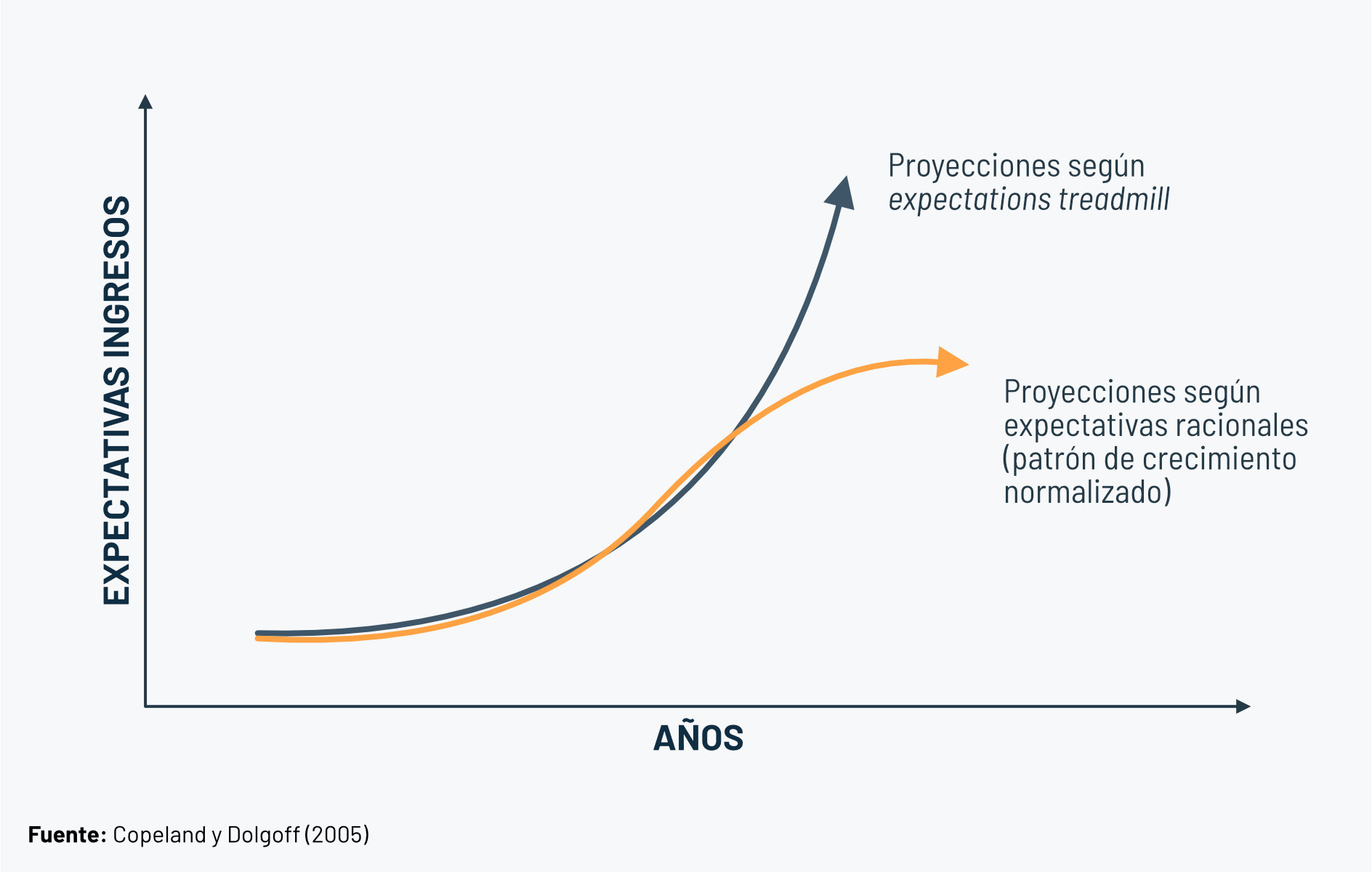

A variant of the previous model is the so-called “Expectations Treadmill” (figure 3) in which analysts and investors, starting from detecting a conservative and systematic policy of formulating Guidance on the part of the listed company, they begin to set their forecasts above those Guidance. This environment of formation of expectations is maintained over time as long as the company exceeds them, until it reaches a point where the company's fundamentals prevent this trend and there is a drastic adjustment in the price (Copeland and Dolgoff, 2005).

It should be remembered that, so important, is that Guidance are well formulated and consistent and credible, such as alerting the market when these internal guidelines or projections are not going to be met, a concept also known as Profit warning. The company's management team should not share projections that they don't really think they can meet, always being transparent and concrete about the risks and uncertainties that incorporate these estimates (Fuller and Jensen, 2002).

For this reason, the quarterly monitoring of the path towards compliance with Guidance, annual or multiannual, should be routine in communicating results in order, when the time comes, to communicate their compliance review or analysis, and before communicating new projections for a new period.

This fact may be one of the reasons that explain the reluctance of managers in some companies to share sensitive information publicly with the market as a whole, as a result of the concern generated by assuming in writing a series of operational and financial objectives or goals that compromise them for the future in the face of the possibility of non-compliance, and therefore of the risk of communicating a possible Profit warning (White, 2020).

In the practice of Investor Relations, the communication of a Profit warning it is considered an exercise in transparency and a test of the company's credibility. The market never welcomes surprises, whether they are good news or bad news, and yet it is willing to reward those companies that are predictable (Fuller and Jensen 2002). Anticipating that the forecasts of results or other variables that were shared with the market a year earlier will not be achieved does not imply Per se the loss of trust in the company, but the market will have to adjust its expectations based on new relevant information. It is true that, if this practice becomes recurrent, either by excess or by default, then we can reach a situation of bankruptcy of trust because the market understands that the company has lost credibility every time it communicates Guidance that never suffices or that always exceeds. In this case, the value can enter a dangerous downward spiral that can be amplified by the activity of short sellers.

In the United Kingdom, the practice of advertising Profit Warnings is very much embedded in the culture of issuers and, of course, in demand by institutional investors.

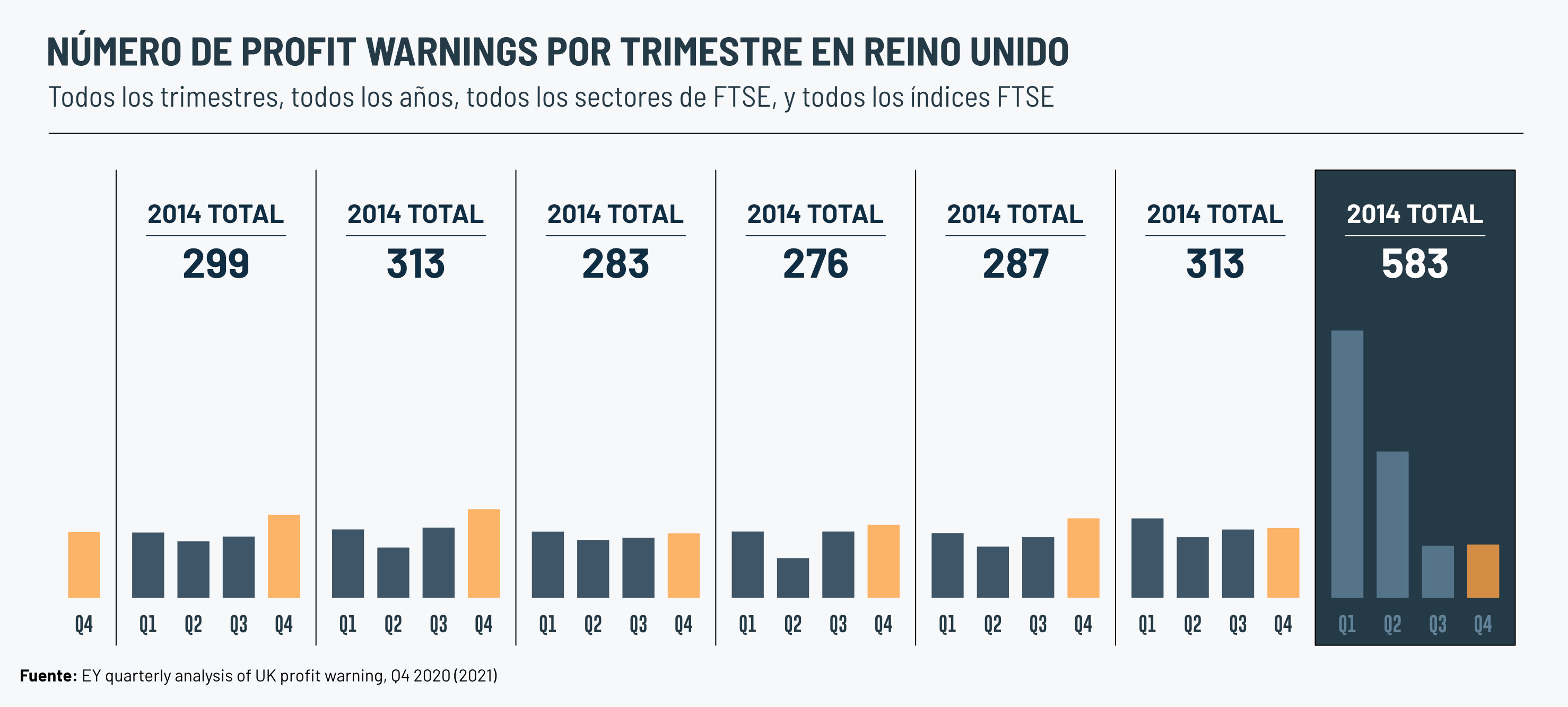

The latest report by the consultancy firm EY on monitoring this aspect highlights how in 2020 an all-time record was reached with more than 580 Profit Warnings press releases, affecting 35% of the total number of British listed companies, a trend that was highly conditioned by the pandemic, since more than 50% of the announcements for the entire year were concentrated in the first quarter (figure 4). However, it is striking to note that in previous years, the volume of these announcements has been very significant and widespread in all sectors of activity listed on the stock exchange. It is, without a doubt, an interesting aspect of Investor Relations management to reflect on, since timely notice can prevent us from a more severe correction than would occur if we waited until the last minute to communicate the final results. In this sense, the capabilities of company information systems have a lot to say when it comes to providing the organization with a sufficient waist to anticipate the market in the face of the forecast of significant deviations from the promises given.

In short, all these considerations regarding the management of Guidance And of the Profit Warnings, are aimed at promoting transparency and credibility when it comes to sharing the company's development prospects, with all the caveats that this implies, in which the Investor Relations function plays an undisputed role.

References

White, F. (2020): Where is the Equity Story of the Spanish listed company? , Studies and articles, Spanish Stock Exchanges and Markets (BME), https://n9.cl/93en1

Copeland, T., and Dolgoff, A., (2005): Outperform with Expectations Based Management, Wiley.

HEY, (2021): EY quarterly analysis of UK profit warning, Q4 2020, Ernst & Young Global Limited, https://www.ey.com/en_uk/strategy-transactions/profit-warnings

Finno, A. and Brush, M. (2013): Guidance Practices and Preferences at NIRI White Paper. National Investor Relations Institute.

Fuller, J. and Jensen, M.C., (2002): Just Say No to Wall Street, Monitor Company and M.C. Jensen.

-

Francisco Blanco Bermúdez

Founding partner of the consultancy firm Sigma Rocket and academic director of the Advanced Investor Relations Course organized by the BME Institute. Doctor in Business Economics with a Cum Laude mention, and a degree in Economic and Business Sciences, both from the UAM, he is considered to be one of the main authorities in the discipline of Investor Relations, both professionally and academically.