The answer, without a doubt, is conditioned by the circumstances of the company involved, since making a statement of progress of financial results does not respond to a regulatory obligation, which certainly does not exist, but rather to an exercise of voluntarism. Therefore, we have to resort to the nuances and unwritten rules of the market to answer this question in the right measure. It is possible that, on some occasions, especially in the process of preparing annual accounts, and less often in the process of preparing quarterly results, a company, in the light of the preliminary results it obtains while the auditing work is being finalized, may be tempted to publish an advance of them to advance good news and thus obtain a positive impact on the price, instead of waiting for the publication of complete, verified and certified financial statements together with the corresponding management report, whose period of time between the two communications may be up to one and a half months in the case of listed companies in the Continuous Market. However, this type of communication initiative, a priori, seems reckless and unnecessary, since advancing some financial variable in isolation, such as turnover or EBITDA, exposes the company to having to provide a series of explanations and details to justify the evolution of these variables that it cannot actually do, because answering the doubts or reasonable queries of investors and analysts in this specific case would mean giving discriminatory treatment and providing non-public privileged information, and in the event of not answering these questions, which would be reasonable, the credibility of your communication policy could be jeopardized when transmitting an objective suspected of impacting the price.

It is easy to understand that behind an operating profitability parameter such as EBITDA there are multiple variables that explain its behavior, both at the level of revenues (prices, volumes, geographical and product markets, regulation, etc.) and of costs, both fixed and variable, which only through comprehensive reporting explained through the management report makes it possible to cover the communication of results in a transparent and effective manner. I insist, it is true that we can anticipate the financial results of a period with two or three parameters, and even advance the forecast for next year with those same parameters, but it is imprudent and above all unnecessary when we are going to do it with the publication of the annual accounts in a safer context and, above all, with greater responsiveness.

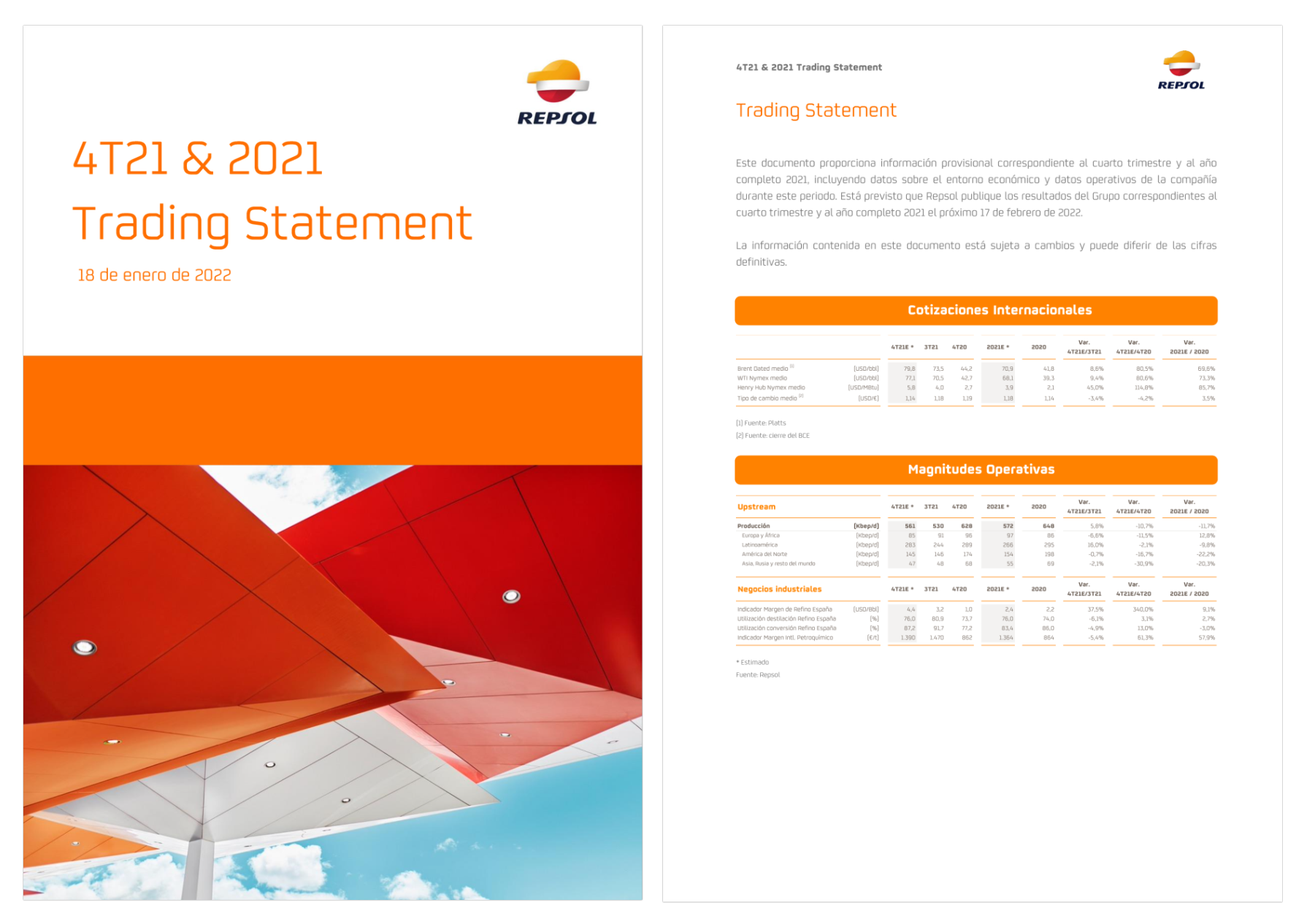

In this regard, it is important not to confuse the publication of an advance in financial results with what some companies do with respect to operating variables of their business or exogenous variables over which they have no influence, but which do condition the evolution of their activities. I am referring, for example, to the case of the so-called “trading statement” that some energy companies, such as Repsol, publish a few days after the quarterly or annual closing, the last one published on January 18, 2022. In this report, Repsol collects at the end of 2021 some fundamental variables of the economic environment and industry, such as the average Brent Dated and the average Henry Hub Nymex as references for the price of crude oil and gas respectively, the evolution of exchange rates, or some operational and non-financial quantities of production (upstream business) and industrial businesses.

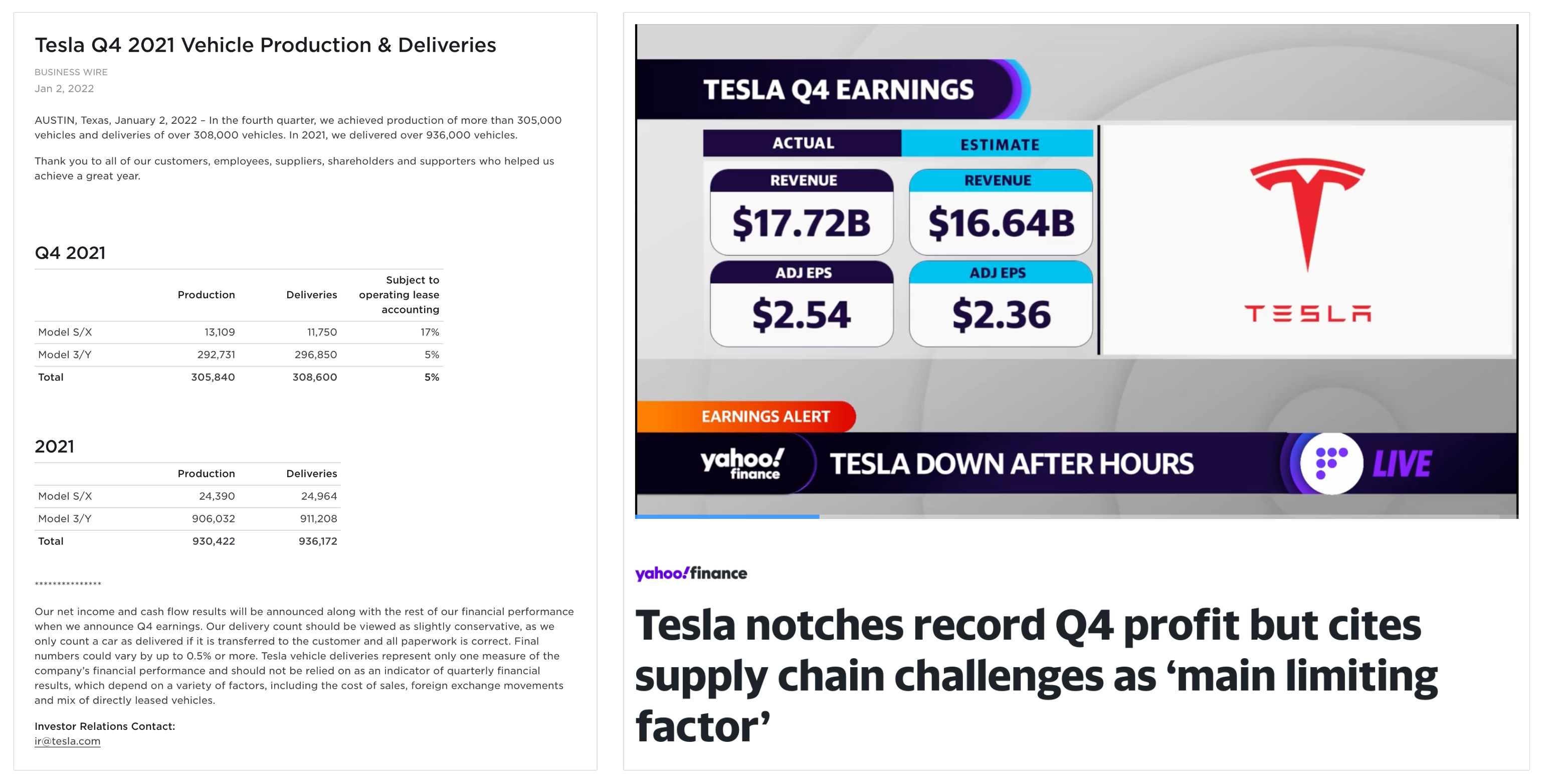

Another interesting example in this regard is represented by Tesla, which on January 2, 2022, published the so-called “state of production and delivery of vehicles” at the end of 2021. As highlighted in its statement, this indicator of vehicle deliveries “represents only a measure of the company's financial behavior and should not be considered as an indicator of quarterly results, which depend on a variety of factors including sales costs, exchange rates and the mix of direct vehicle renting”. In fact, the company reserved for the release of results on January 26, 2022, the pertinent explanations about the evolution of management in the past financial year 2021, as well as its forecast for the current one, in which it warned, among other things, of its negative perspective on problems in the supply chain as a result of the chip crisis, an effect that the market soon discounted.

What is the purpose of this type of “leading indicator” press release? Precisely that, to anticipate the economic and operational context in which the company's activity has been carried out to avoid speculative movements in the stock markets, prior to the communication of financial results, as is the case with certain short film activity, a fact that also facilitates the beginning of periods of Blackout to avoid possible practices of Insider Trading. In this regard, it is important to highlight how in these two cases of Repsol and Tesla, in line with their announcements of advanced indicators, both companies also anticipate to the market the next date of official publication of the company's economic-financial results corresponding to the last management period, while however, this practice is not identified in any recent case of an announcement of progress of financial results. This is why we say that often the differences in the quality of Investor Relations lie in the nuances that respond to unwritten rules and experience that directly affect credibility.

Of course, there may be exceptional cases in which it is necessary to anticipate some type of financial trend to the market. This is the case of Profit Warnings, such as the one announced by Siemens Gamesa on January 20, 2022, in which it advanced results for the first quarter of 2022 and the modification of Guidance of the 2022 financial year as a result of greater than expected disruptions in the supply chain. With this, the company intends, with good vision, to reduce the negative impact of the element of surprise that would entail waiting at the end of the year to fail to meet annual objectives.

If the question is to reduce publication times since the end of the management period, then the important thing is to have well-oiled information systems and ERPs with reliable verification processes that allow you to measure publication times as much as possible, as CaixaBank has achieved, for example, that this year it published its annual results for 2021 less than a month after closing.

In conclusion, we understand that the possibility of anticipating some unaudited financial figures that show positive management results is a tempting idea that is not without controversy, and that it has nothing to do with objectives of systematic and transparent communication to the market. Perhaps in this context, when companies are in the process of preparing their annual results report for 2021, it is worth remembering the popular saying that “not for long does it get up early”.

-

Francisco Blanco Bermúdez

Founding partner of Sigma Rocket